NFT Lending: How I made a small fortune in the bear market

Happy w/ 7% a year? Get in, loser. We're going 100%+ APY 🤝

I made more money than I earned last year. How? Why, w/ NFT lending, of course 🧠

NFT lending protocols are becoming popular staples of every major chain today. They first exploded on Solana, w/ Sharky.fi. Similar lending mechanics were introduced to Blur afterward, w/ Blur Blend. Then came Liquidium, the first DeFi protocol on Bitcoin, which also happens to be an ordinal lending platform, and it’s about to bust out of beta in a major way.

Let’s take a look at how NFT lending works, and I’ll share my personal experiences, what I’ve learned while averaging 160% APY on Sharky.fi, and any thoughts that might help you if you want to run lending.

But first… why lend? Why not borrow?

Credit makes the world go brrr.

Always been that way. From the polished Venetian bankers to the lavish Buddhist temples in China that would put up their temple gold as collateral for loans, this is how creditors around the world accumulated capital, and thus power, throughout history. (An exceptional read on this subject is David Graeber’s “Debt: The First 5000 Years”.)

Lenders lend and usually win. Borrowers borrow and take on a lot more risk, and sometimes they win, sometimes they lose. Another way to look at lending vs. borrowing is to see it in a similar dynamic to shorters vs. long traders: They’re opposite sides of the same coin, engaged in a pvp battle.

Still, in lending vs. borrowing, the game isn’t necessarily zero sum, and that’s the fundamental difference. In a lender’s market, both parties can come out on top, and that’s the appeal for the borrower: The opportunity cost of capital.

Let’s look at an example:

An NFT project is about to drop. Bob is convinced it’ll pump, and he’s got 5 whitelist spots. He posts an NFT he wants to put up as collateral. Alice sees the post, and accepts the loan terms. (i.e., Bob secures the loan against his NFT, which he would lose to Alice if he fails to pay up within the agreed-upon deadline.)

Bob borrows the sum he needs, he mints, and if his hypothesis is correct, he flips for a healthy profit, pays Alice back the loan (w/ interest), and pockets the profit.

Win-win 🤝

But you see what the problem is here, specifically for the borrower? Their gamble has to be right, so they are technically taking on the bigger risk. (Technically, Bob also gets the bigger reward, but Alice can just sit back and lend funds to many Bobs at a time, thereby being able to accrue some serious capital w/o having to incur additional risk.)

Alice gains something either way, even if Bob fails to pa

y back. The only real issue crops up in times of significant and sudden market downturns, which I’ll cover later on.

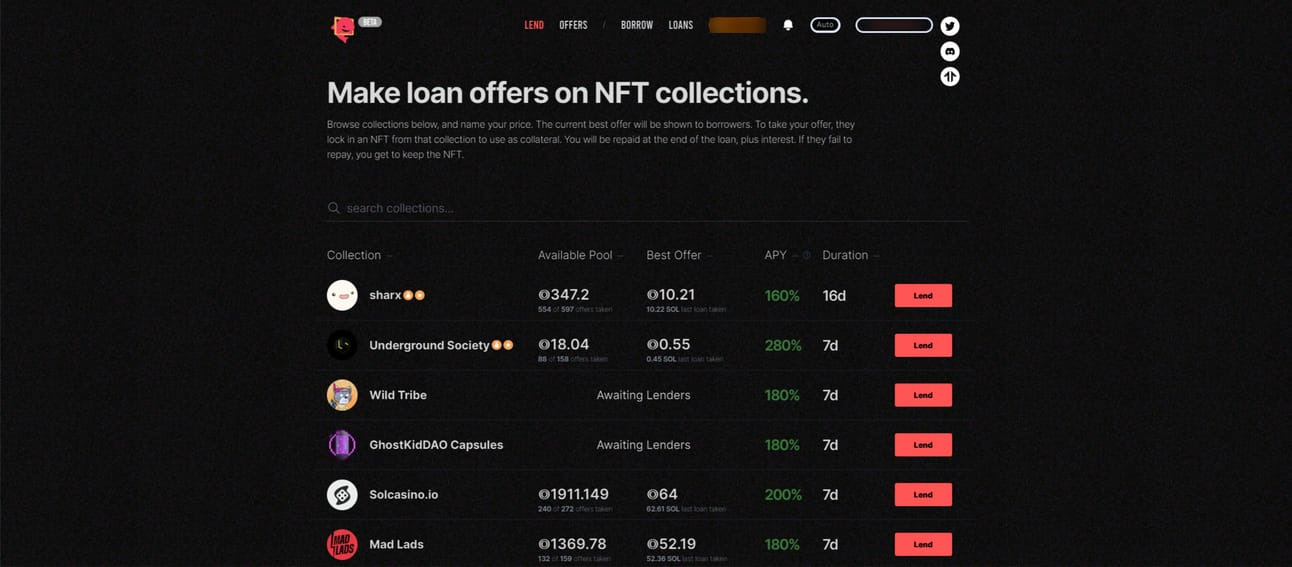

But rn, let’s take a look at Sharky lending real quick.

NFT Lending on Solana: Sharky.fi

For this piece, I wanted to focus on Sharky for several reasons:

It’s the best lending protocol out there so far. (I’ve used Blend. Not impressed.)

Liquidium isn’t open to the public, and it’s early days. (I’m also an angel investor in Liquidium, w/ beta access, but it’s not there yet. Liquidium will get there, and it’s building rn during the bear. Remember: Sharky has roughly 1 year on both of these apps.)

Long term, Liquidium on Bitcoin will be amazing, but again, on Bitcoin. If you want to lend only on Bitcoin, that’s fine too, but I like to diversify and make sure my bags are active as much as possible to accumulate more capital.

Sharky has the best loan conditions out of any app out there. It’s also the easiest tool to use, easy to understand, easy UX, everything easy 🤙

Unfortunately, Sharky is on Solana only, and that’s fine. I am long-term bullish on $SOL b/c Solana has a few compelling use cases, like if it pivots to a casino/gambling chain w/ gaming, then it could become one of the best chains in the world, w/ opportunities to onboard the masses. (Normies may have an irrational hatred toward blockchains, but they sure do love gambling.)

“Sounds perfect! Where do I sign up?”

Not so fast.

NFTs on Solana: The collateral problem

Top 5 Solana projects based on 30-day window

This issue isn’t unique to Solana anymore. It’s no secret that we’re in an NFT bear market. In fact, this is the worst one I’ve experienced thus far.

Point is, it’s harder to determine what is “safe” to take as collateral rn. However, when there’s blood, that’s typically the best time to buy, and it also happens to be the best time to loan. (Scared money don’t make money.)

So if you’re still good w/ your conviction bets, look for projects you believe in on Solana. (rn, I’m liking Sharky, Solcasino, and Vtopia.)

In other words, you have to be good w/ 2 factors:

You’re bullish on $SOL.

You’re bullish on specific NFT projects on Solana that you can accept as collateral.

Still here? Good. Now let’s talk about the main risk.

Lending: The worst risk factor is… ⚫🦢

Market downturns suck, but they can suck especially for lenders. That’s b/c you might have a considerable number of defaults on your hands, so you end up w/ lower liquidity and a bunch of NFTs.

This happened to me during the FTX crash. I ended up “losing roughly 400+ $SOL”, w/ 4 t00bs defaulted, at 80 sol each.

Yeah. You read that right. Just a few weeks later, they were trading at upwards of 200 sol. Had I chosen to sell the t00bs, I would’ve nearly doubled my capital sum. This is why investing in blue chips/conviction bets is imperative, or you risk getting wiped out.

At this point, you can either choose to hold onto your collateral, since, w/ a price crash, what you’re getting are these NFTs at a discount. Since you believe in their long-term value as a holder, you should be comfortable holding until prices pump back up, and further.

This factor also depends on your time horizon: Do you want a quick flip for more liquidity? Or would you like to diversify and hold? As you can see, the lender’s got options, and optionality always wins 🤝

Thoughts on lending via Liquidium and Blend

It’s funny. I’ve only ever acted as a lender on Solana. But on Ethereum? I’ve never been a lender. I’ve used Blend a couple times, once w/ my Beanz and another w/ my Pengu, and I defaulted on purpose both times.

Why is lending on Ethereum not appealing? Is it b/c of all the exorbitant gas fees that make me want to spoon my eyes out? Probably. How much am I really making if I have to pay, say, $30 in gas fees and the interest is very little?

Another issue is that Blend offers perpetual lending w/ 0% interest. Unlike Sharky, it does not offer fixed terms. This means that the risks—as well as the rewards—are not as clear, hence introducing conditions of uncertainty I’m not comfortable operating under.

While writing this part, I toyed w/ the idea of testing lending on Ethereum, but I’ll pass for now. Gas fees are way high 😂

From broke to lender extraordinaire

If I’ve done my job correctly, you should be convinced that being a lender is an awesome way to snowball your bags and accumulate more capital. Lending is my main DeFi play, and I’m hoping that an amazing lending platform comes to Ethereum eventually. For now, I’m sticking to Solana (Sharky) and Bitcoin (Liquidium) lending.

So… you in?